Where is it going and is it appropriate?

A ~$40bn Market That “Just Worked”

Aussie bank and financial hybrids were a ~$40bn market when APRA called time on new Alternative Tier 1 issuance.

This is what we call AT1 capital in a bank’s capital structure.

Beyond my Master’s syllabus, my first real exposure to these was working as an analyst at a boutique fund manager on Collins St back in 2014. We were running dedicated portfolios purely in hybrid securities for clients in pension phase.

They paid ~3.3% above BBSW, fully franked, so ~7–8% grossed-up.

And importantly, they just… worked.

Even through GFC and COVID, they kept paying. Structurally (dividend stoppers, etc.), they gave investors a level of confidence around income that was hard to replicate elsewhere. For HNW/UHNW clients sitting on cash in pension phase, this was ideal, especially when term deposits were ~3% p.a..

Clients would live off the distributions, trim positions at year-end to manage tax, and move on.

Simple.

Even though we weren’t massive (~$500m FUM), we were still one of the larger participants in the hybrid market. Because for that cohort, hybrids solved a very specific problem:

Consistent, tax-effective income with minimal perceived volatility.

The Rotation Has Already Started

We’ve already seen approximately ~$4.6bn of capital returned via:

– ANZ Capital Notes 2 (~$1.5bn, December 2024)

– CBA PERLS X (~$1.365bn, April 2025)

– Westpac Capital Notes 5 (~$1.69bn, September 2025)

The obvious first destination has been Tier 2 subordinated debt via ETFs such as VanEck’s SUBD, BetaShares’ BSUB and Macquarie’s MQSD, with roughly ~$1.8bn absorbed.

But this is not a clean reallocation, it is only the first leg of the rotation.

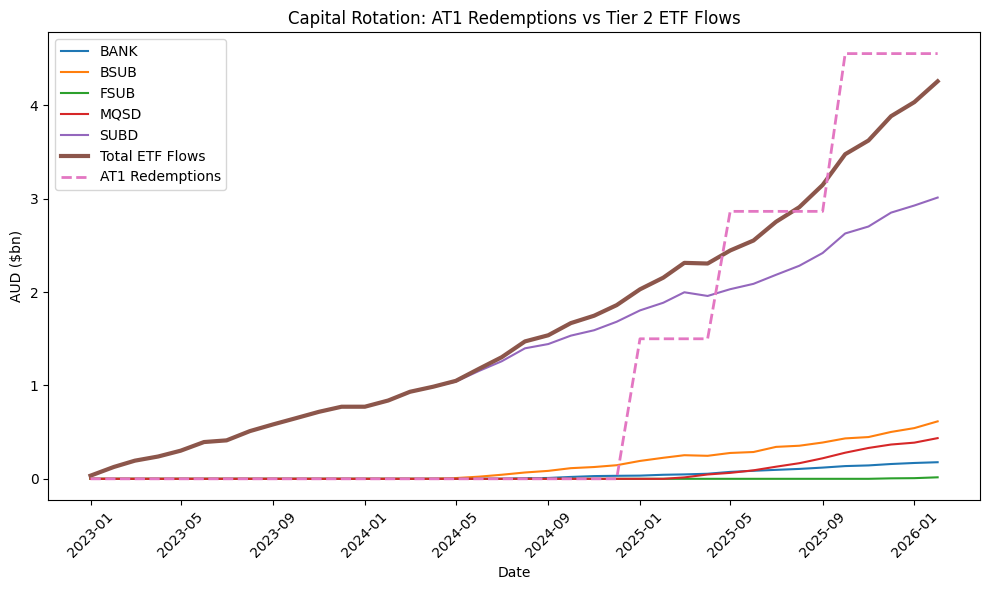

What the Data Actually Shows

Figure 1: Capital Rotation – AT1 Redemptions vs Tier 2 ETF Flows

Source: ASX

Flows into these products started building before the redemptions hit.

This wasn’t just redeployment, it was pre-positioning.

But when the redemptions occur, they come in steps, whilst the market absorbs capital gradually.

Not one-for-one and not instantly.

From Product Allocation to Portfolio Construction

Hybrids solved income, tax efficiency, liquidity and accessibility in one instrument.

Now that outcome has to be constructed. This is no longer a simple rebalance.

To achieve a similar risk/return profile, advisers must blend across the capital structure, reintroduce franking where relevant, manage liquidity trade-offs, and align with client lifecycle constraints. Because for many pension-phase investors, private credit is not a clean substitute.

The good advisers will reallocate. The great ones will reconstruct.

The Great Opportunity

If the first phase of this cycle is about understanding where capital is going, the next phase is about recognising how much is still to come.

What we’ve seen so far is only the beginning.

The ~$4.6bn that has already rolled back into the market is a fraction of the total.

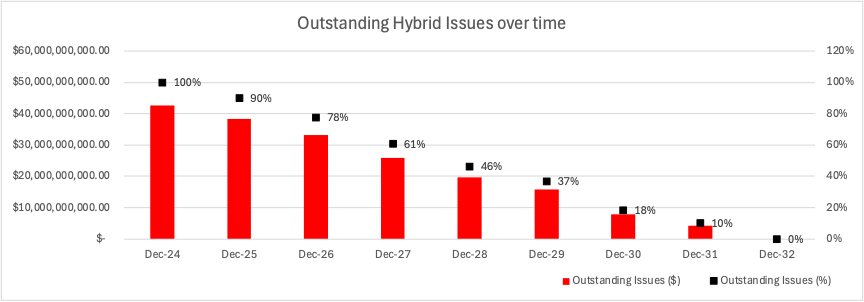

Figure 2: AT1 Size of Outstanding Issues from time of APRA Announcement year-on-year forecast

Source: ASX

Based on the current maturity profile of outstanding bank hybrids, close to 50% of the ~$40bn market is expected to roll off after year three of the rolloff period.

That is a significant wall of capital. And importantly, it doesn’t come back evenly. It comes back in waves, which means the market isn’t just dealing with a reallocation problem today. It’s dealing with a multi-year capital recycling event.

Short term, we are seeing pre-positioning and early flows into Tier 2. Medium term, we will see larger volumes of capital returning and greater dispersion across asset classes.

There is no single domestic market large enough or structurally similar enough to absorb this capital in one place.

Tier 2 helps, but it isn’t sufficient. Private credit may absorb some, but may introduce a multitude of different risks. Equities recover franking, but increase volatility.

As more capital comes back, dispersion increases, not concentration. This creates a structural gap between demand and available solutions. That gap presents a clear opportunity for advisers to construct portfolios deliberately.

This same gap also represents a clear opportunity for product issuers and active managers to design solutions that better replicate the hybrid outcome. Because with nearly half the market still to roll off, the real opportunity hasn’t even started yet.

The Structural Gap That Is Emerging

Hybrids packaged a complex outcome into a single instrument.

What we now have is a fragmented set of building blocks. This creates a clear opportunity for active managers and product issuers.

Because, right now, we are not replacing AT1 hybrids.

We’re just approximating them.